…CBN Pushes Industry-Wide Security Reforms

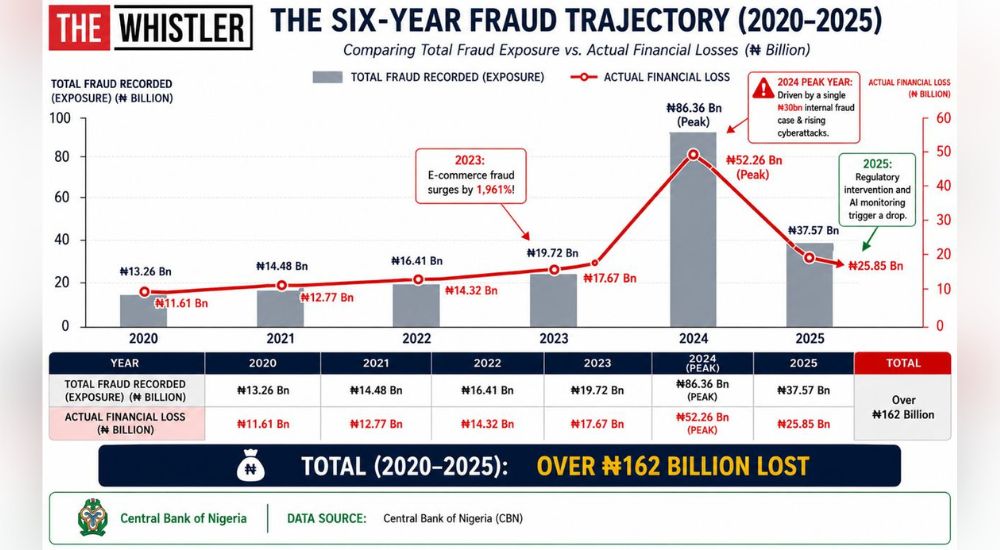

Nigeria’s financial system lost more than N162bn to fraud between 2020 and 2025, according to Central Bank of Nigeria (CBN)-supervised industry data, reflecting sustained pressure on the country’s banking infrastructure as both fraud attempts and actual losses continued to rise over the six-year period.

The data shows that while total fraud recorded across banking channels increased significantly, actual financial losses also remained high, underscoring the difficulty in fully containing fraud risks within Nigeria’s rapidly expanding digital financial ecosystem.

Across the period under review, the total fraud amount rose from N13.26bn in 2020 to N86.36bn in 2024, before declining to N37.57bn in 2025. At the same time, the amount involved or actually lost moved from N11.61bn in 2020 to N52.26bn in 2024, before easing to ₦25.85bn in 2025.

In 2020, fraud activity was already widespread across multiple channels, including ATM withdrawals, over-the-counter banking, cheque transactions, mobile banking, internet banking, POS terminals, and emerging e-commerce platforms. Total fraud stood at N13.26bn, while N11.61bn was lost, indicating that a large share of attempted fraud translated into actual financial exposure.

By 2021, total fraud rose to N14.48bn, with N12.77bn lost, driven largely by increased POS-related fraud incidents. Industry data during the period showed a sharp rise in POS fraud activity, even as some web-based fraud cases declined.

In 2022, fraud exposure increased further to N16.41bn, while actual losses rose to N14.32bn. The year was characterised by a rise in corporate card fraud and a significant increase in ATM-related fraud, even as mobile, POS, and web channels recorded some moderation.

The upward trend continued in 2023, when total fraud climbed to N19.72bn, with N17.67bn lost. This increase was largely driven by a surge in e-commerce fraud, which reportedly rose by 1,961 percent, highlighting the growing exploitation of online payment platforms and digital retail systems.

The most significant shift occurred in 2024, when fraud levels surged sharply to N86.36bn, while N52.26bn was lost. This represented the peak of the six-year period and was largely attributed to a major internal fraud case estimated at about N30bn, alongside increased cyber and web-based fraud incidents.

The data also suggests a widening gap between fraud attempts and actual losses, indicating both higher attack volumes and improved detection mechanisms.

In 2025, the trend reversed slightly, with total fraud declining to N37.57bn, while actual losses fell to N25.85bn. The reduction has been linked to improved regulatory oversight by the Central Bank of Nigeria, stronger fraud monitoring systems within financial institutions, enhanced customer verification processes, and increased collaboration across the banking industry.

Despite this improvement, the 2025 figures remain significantly higher than pre-2023 levels, indicating that fraud risks are still elevated across Nigeria’s financial system.

Over the six-year period, fraud was consistently recorded across multiple banking and payment channels, including ATM networks, mobile banking applications, internet banking platforms, POS terminals, cheque systems, over-the-counter transactions, and e-commerce services.

The pattern reflects a gradual shift in fraud tactics as criminals increasingly exploit both traditional banking systems and digital platforms.

The Central Bank of Nigeria has responded with a series of reforms aimed at strengthening transaction monitoring, improving compliance standards, and enhancing cybersecurity across financial institutions. These efforts have contributed to recent improvements, particularly in electronic payment systems.

However, despite these interventions, fraud remains a persistent structural challenge. The data shows that both fraud attempts and actual losses have grown substantially over the period, driven by increased digital adoption, expanding transaction volumes, and evolving criminal tactics.

Overall, the six-year data paints a picture of a financial system under sustained fraud pressure, with over N162bn recorded in fraud exposure and actual losses between 2020 and 2025.

While recent improvements are evident, the broader trend underscores the need for continuous innovation in fraud prevention, stronger enforcement, and sustained collaboration between regulators and financial institutions.

The Central Bank of Nigeria Governor, Olayemi Cardoso had last week said the apex bank is targeting a significant reduction in digital payment fraud, with a goal of lowering fraud losses to less than 0.001 per cent of total transactions by 2028.

He said the initiative would be supported by stronger integration of the Bank Verification Number system, identity management platforms and artificial intelligence-powered fraud detection tools.

“People’s money must be safer in the digital system than under their mattress. A payment system is only as strong as the trust people have in it,” he stated.

The governor further highlighted the potential of Nigeria’s open banking framework, noting that more than 100 licensed application programming interfaces (APIs) are already available to support innovation and the growth of globally competitive fintech businesses.

The Payments System Vision 2028 is designed to improve payment efficiency, strengthen resilience, encourage innovation, expand financial inclusion and deepen Nigeria’s integration with regional and global payment systems.

Cardoso said efficient payment systems would lower transaction costs, boost transparency, help businesses access new markets and support economic growth.

“As the Federal Government builds roads, schools and hospitals, we must also build the invisible roads that move money,” he said.

Describing the initiative as a collective national project, he called on banks, fintech companies, regulators, technology providers and development partners to collaborate in delivering its objectives.

“Vision 2028 is not a government project. It is a Nigerian project,” he added.