Between 2010 and 2019, Ethiopia experienced one of the fastest expansions of foreign direct investment (FDI) in Sub-Saharan Africa, driven by state-led industrialisation, infrastructure megaprojects, and manufacturing zones.

At its peak, Ethiopia was widely described by international financial institutions as one of Africa’s most promising frontier investment destinations. Between 2010 and 2019, Ethiopia was widely regarded as a frontier investment success story. According to the World Bank and IMF macroeconomic datasets, the country recorded average GDP growth of around 9% annually during the decade before COVID-19, driven largely by state-led infrastructure expansion and rising foreign direct investment (FDI).

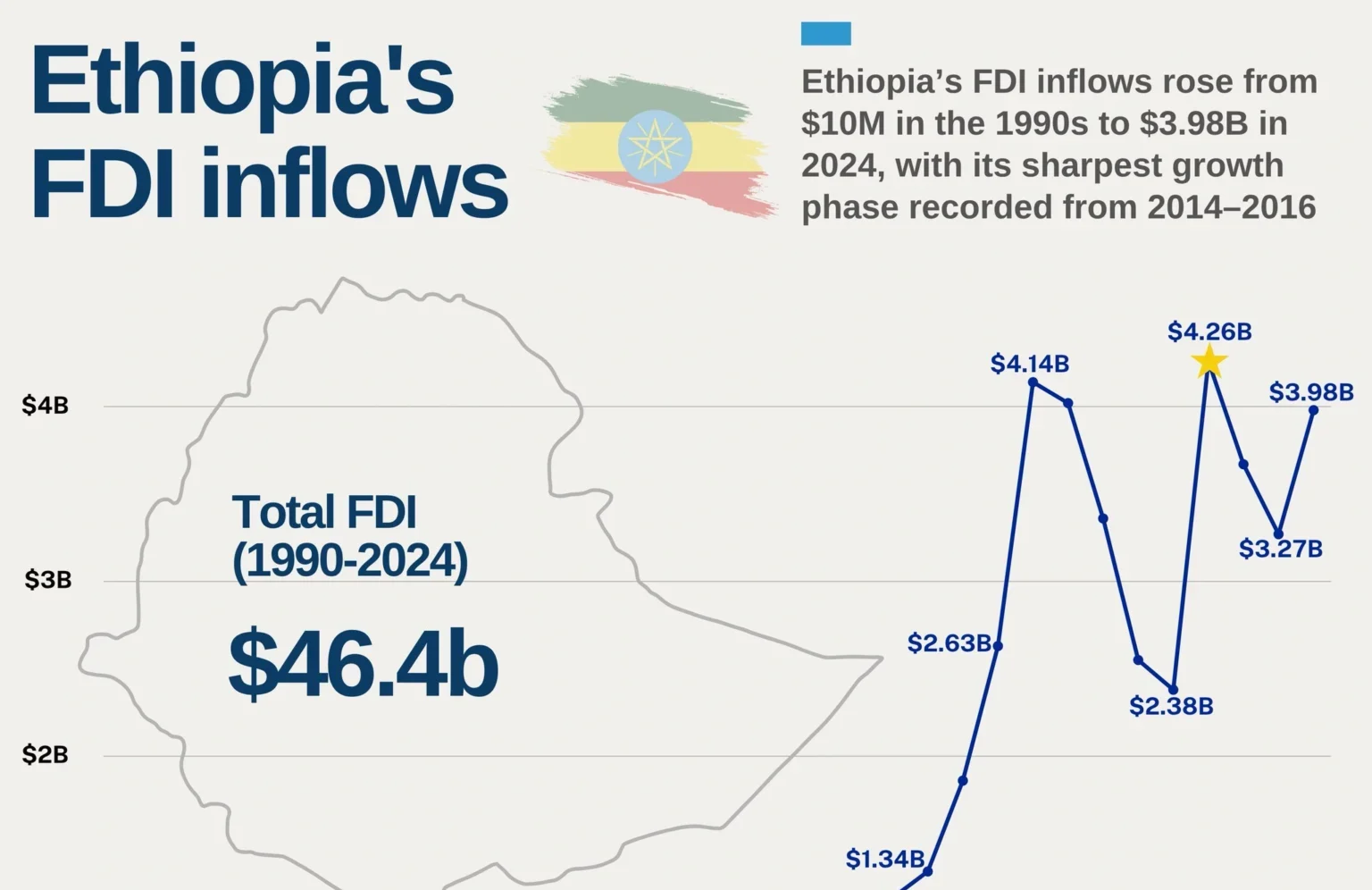

Between 2010 and 2019, the country experienced one of the fastest expansions of foreign direct investment (FDI) in Sub-Saharan Africa, driven by state-led industrialisation, infrastructure megaprojects, and manufacturing zones. According to the World Bank’s development indicators, Ethiopia’s FDI inflows rose from less than $1.1 billion in 2010/11 to over $4 billion by 2016/17, marking one of the steepest investment growth curves in Africa during that period.

By 2021, inflows reached approximately $3.9 billion, partly boosted by Ethiopia’s telecom liberalisation and the entry of Safaricom into the market. The UNCTAD World Investment Report 2023 further confirms Ethiopia’s position as a key investment hub in East Africa, recording $3.7 billion FDI inflows in 2022, though already showing a downward trend from previous years.

Yet beneath this upward trajectory, a structural vulnerability was forming, one that would become visible after 2020.

The outbreak of the Tigray conflict in 2020, followed by continued instability in parts of Amhara and Oromia, fundamentally altered investor risk calculations. The 2022 Center for International Private Enterprise (CIPE) assessment shows that real sectors of the economy have been significantly affected by the conflict. Medium, Small, and Micro-Sized Enterprises (MSMEs) operators in all regions have informed us that they have either reduced their operations significantly (by 60-80%) or shut their businesses down.

A 2024 macroeconomic profile of Ethiopia notes that FDI inflows dropped during periods of instability, particularly where industrial parks and transport corridors were affected by insecurity and logistical disruption.

Satellite-based research on conflict-affected regions of Ethiopia shows that even when agricultural production remained resilient, broader economic systems, including logistics and market access, were heavily disrupted during conflict periods.

An investment analyst, Mesfin Menza, quoted in a World Bank–linked policy review summarized the shift bluntly:“ Conflict risk is not only about destruction, it is about repricing the entire investment environment, from insurance premiums to supply chain predictability.”

Ethiopia’s industrial parks; once marketed as engines of export-led growth became a central indicator of this shift. The Hawassa Industrial Park, one of Africa’s flagship textile export zones, faced factory closures and job losses after Ethiopia lost preferential access to the U.S. market under the African Growth and Opportunity (AGOA) restrictions linked to the conflict. At its peak, the park employed more than 35,000 workers, but experienced significant disruptions during 2022–2023 due to market access restrictions and investor withdrawal pressures.

Consistent with this, Ethiopia experienced significant economic setbacks following the suspension of AGOA in January 2022, according to the African Development Bank Group’s (AfDB) Country Focus Report 2025. The report highlights that Ethiopia’s manufacturing economy has taken a significant hit since its suspension from AGOA.

The World Bank’s industrialisation assessment report highlights that Ethiopia’s industrial model is highly sensitive to external shocks, particularly those affecting export logistics and political instability.

A factory supervisor at an industrial zone in Oromia Mrs Alemitu (name withheld for safety reasons) described the operational reality as: “We can produce. But uncertainty kills contracts. Buyers don’t wait when there is conflict risk.”

While Ethiopia maintained relatively strong FDI inflows compared to regional peers, the UN Trade and Development (UNCTAD) and UNIDO trend shows volatility:2016/17: ~ $4.1 billion peak growth phase, 2019/20: ~ $2.4 billion decline due to instability and COVID-19 shocks, 2021: rebound to ~$3.9 billion, 2022: decline to ~$3.7 billion.

The UNCTAD World Investment Report confirms that global FDI fell by 12% in 2022, but stresses that instability disproportionately affects fragile economies already dependent on external financing.

According to UNCTAD/World Bank data Ethiopia’s FDI inflows peaked at more than $4 billion in 2016–2017, declined to about $2.4–2.5 billion by 2019–2020, and later recovered to nearly $4 billion in 2024.

The Ethiopian Investment Commission also reported FDI inflows of approximately $3.82 billion during the 2023/24 Ethiopian fiscal year, consistent with the UNCTAD trend.

While there are signs of slow recovery in 2025 and 2026, with inflows rising slightly, the overall trend paints a grim picture.

Despite the marginal increase in capital inflows, Ethiopia still grapples with the FDI challenges due to the ongoing regional conflict and unstable political environment.

A senior African development economist, Pierre Nguimkeu, Director of the Africa Growth Initiative (quoted in a Brookings-style policy briefing) noted:“ FDI does not disappear in conflict economies; it becomes selective, risk-sensitive, and concentrated in extractive or highly secured sectors.”

Before 2020, Ethiopia’s investment story was driven by: Industrial parks expansion, Infrastructure megaprojects, Chinese-financed railways and energy systems, Liberalisation of telecom and logistics.

After 2020, the narrative shifted to security risk premiums, currency shortages, contract uncertainty and Investor hesitancy.

A policy analysis by international development institutions notes that Ethiopia’s investment performance remains structurally strong but increasingly constrained by non-economic risks, including governance and conflict exposure.

Across Africa, research by UNCTAD and development agencies shows that: countries experiencing conflict see longer FDI recovery cycles, Infrastructure and manufacturing FDI are the most sensitive to instability. Investors increasingly prefer “politically insulated” sectors such as digital services or extractives. Ethiopia now reflects this broader continental trend where investment inflows continue, but confidence becomes uneven.

At the edge of Hawassa Industrial Park, sewing machines hum in long warehouse halls where thousands of young workers stitch garments destined for Europe and the United States. Outside the gates, buses arrive before sunrise carrying mostly young women from surrounding rural towns.

For many workers, this is the promise of Ethiopia’s industrial transformation. For others, it is also where the debate over FDI becomes most visible in everyday life.

Ethiopia’s industrial park strategy, launched in the mid-2010swas designed to shift the country from an agrarian economy into a manufacturing hub. The World Bank and government planners positioned it as a flagship export-led growth model. But nearly a decade later, Yohannes Ayele and Sherillyn Raga, Senior Research Officers at ODI, explain that the model now sits at the intersection of job creation, debt exposure, and what governance scholars describe as “corrosive capital” dynamics: investment flows that generate growth but may weaken long-term sovereignty, transparency, and local value capture.

Hawassa Industrial Park is often cited as Ethiopia’s most advanced eco-industrial zone. According to the Industrial Parks Development Corporation (IPDC), the park hosts more than 20 foreign firms and has created tens of thousands of jobs, mainly in textiles and garments.

In official framing, industrial parks are a success story: export earnings, industrialisation, and foreign exchange generation.

But independent assessments suggest a more complex picture.

A 2023 UNDP economic review notes that Ethiopia’s manufacturing sector remains “weak relative to services growth,” despite years of industrial park expansion and foreign investment inflows.