Most people start investing with the same instinct: find something that goes up and put money in it. That works occasionally. What does not work is doing it without a structure, because when markets turn, a single concentrated position can erase months of gains. Diversification is the antidote, but it is not just about owning more things. It is about owning the right mix of things that do not all fall at the same time. This article walks through the practical strategies beginners can use to build an investment portfolio that holds together under pressure.

Start With Your Risk Profile, Not With Assets

Start With Your Risk Profile, Not With Assets

Before picking a single stock or bond, you need to answer one honest question: how much loss can you handle without selling in a panic? This is not a philosophical exercise. It determines everything about how your portfolio should be structured.

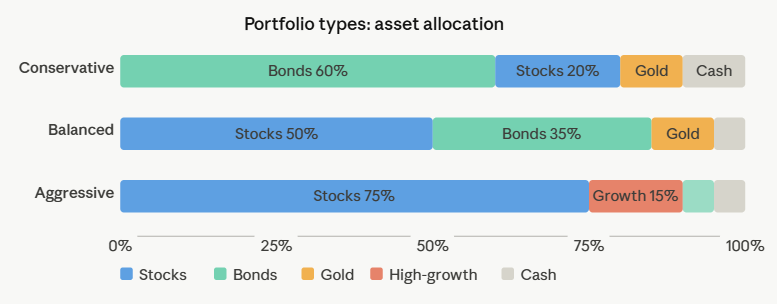

There are three basic portfolio types. A conservative portfolio puts capital preservation first. Most of it sits in bonds, gold, and cash-like instruments. Returns are modest but steady, usually just ahead of inflation. A balanced portfolio splits roughly half into equities and half into bonds and real assets. Returns are higher, but drawdowns during bad years are too. An aggressive portfolio leans heavily into equities, often 70% or more, including growth stocks or higher-risk sectors. The upside is significant over long horizons. So is the pain during corrections.

Your choice should also reflect your time horizon. If you need the money in two years, aggressive is the wrong answer regardless of your confidence in the market. The LiteFinance guide recommends a minimum three-year horizon for any serious investment portfolio. Shorter than that, and volatility starts working against you.

The Core Principle: Low Correlation Between Assets

Diversification only works when assets do not move in lockstep. Owning ten tech stocks is not diversification. They tend to fall together when the sector corrects. Real diversification means combining assets whose returns are weakly correlated or even move in opposite directions.

The classic example is equities and bonds. When stocks fall sharply during a recession, investors often move into government bonds, pushing bond prices up. The two assets partially offset each other. Adding gold strengthens this further. Gold tends to hold or rise during periods of currency stress or geopolitical uncertainty, precisely when equities struggle.

Real estate and commodities add another layer. Their returns are driven by different factors: rent levels, construction cycles, supply and demand in physical markets. These do not respond to the same triggers as a tech earnings report.

The practical takeaway: before adding any asset to your portfolio, ask not just whether it might go up, but how it tends to behave relative to what you already own.

Building the Portfolio Layer by Layer

A beginner portfolio does not need to be complicated. Three layers cover most of what matters.

The first layer is the foundation: broad equity exposure through index funds or ETFs that track major markets like the S&P 500 or a global equity index. This gives you participation in long-term economic growth without trying to pick individual winners. It is low cost, easy to maintain, and historically reliable over time horizons of five years or more.

The second layer is stability: bonds, either government or high-grade corporate. These reduce volatility, generate regular income, and provide something to rebalance from when equities fall and become cheap. The share of bonds in your portfolio should roughly increase as your time horizon shortens.

The third layer is protection and alternatives: gold, real assets, or a small allocation to commodities. These hedge against inflation and currency risk. During periods when both stocks and bonds struggle, which does happen, these assets often hold their value.

The table below shows how these layers shift across the three main portfolio types:

| Asset class | Conservative | Balanced | Aggressive |

| Stocks / equity ETFs | 20% | 50% | 75% |

| Bonds | 60% | 35% | 5% |

| Gold / commodities | 10% | 10% | 5% |

| Cash / short-term | 10% | 5% | 5% |

| High-growth / alternatives | 0% | 0% | 10% |

These are starting points, not rules. Your actual allocation should reflect your goals, timeline, and how you personally handle a 20% drawdown.

Rebalancing: the Maintenance Work That Most People Skip

Rebalancing: the Maintenance Work That Most People Skip

A portfolio that is not rebalanced drifts. Equities grow faster than bonds in bull markets, so after a few good years your 50/50 split quietly becomes 70/30. You are now carrying more risk than you intended without making a conscious decision to do so.

Rebalancing means periodically selling what has grown above your target allocation and buying what has fallen below it. Annually is the most common approach and works well for most investors. Some rebalance when any asset class drifts more than five percentage points from its target.

The counterintuitive part is that rebalancing forces you to sell high and buy low automatically. When equities have a strong year, you trim them. When bonds lag, you add to them. This mechanical process imposes discipline that most people cannot maintain emotionally.

Reinvesting dividends and interest into underweighted assets is a low-friction way to rebalance without triggering large tax events from selling. Over long periods, this compounding effect adds meaningfully to total returns.

Common Mistakes Beginners Make

The most frequent error is over-concentration in familiar names. Investors load up on companies they know and use every day, their phone manufacturer, their bank, their favorite retailer. It feels rational. The problem is that these companies often operate in correlated sectors and respond similarly to economic shocks.

The second mistake is ignoring costs. An ETF with a 0.05% annual fee and one with a 0.95% fee look similar on a chart today. Over twenty years, that difference compounds into a meaningful gap in final returns. Keep costs low, especially for the foundation layer.

The third mistake is reacting to short-term noise. A well-built diversified portfolio will underperform during certain periods compared to a concentrated bet on whatever is hot right now. That is by design. The goal is not maximum return in any single year. It is the best return you can sustain over your full investment horizon without selling in a panic at the wrong moment.

Conclusion

Portfolio diversification is not complicated, but it does require being honest about your goals and sticking to a structure when markets get uncomfortable. Start with your risk tolerance and time horizon. Build three layers: growth assets, stability assets, and protection assets. Choose them based on low correlation, not just recent performance. Rebalance at least once a year to keep the allocation on target. And resist the urge to chase last year’s winners. The portfolios that compound quietly over time tend to outperform the ones built around excitement. The structure is what makes it work.